Lessons from the Homeplus Crisis: How a ₩7.2 Trillion Retail Giant Ended Up in Court-Led Rehabilitation

Have You Been Following the Homeplus Story?

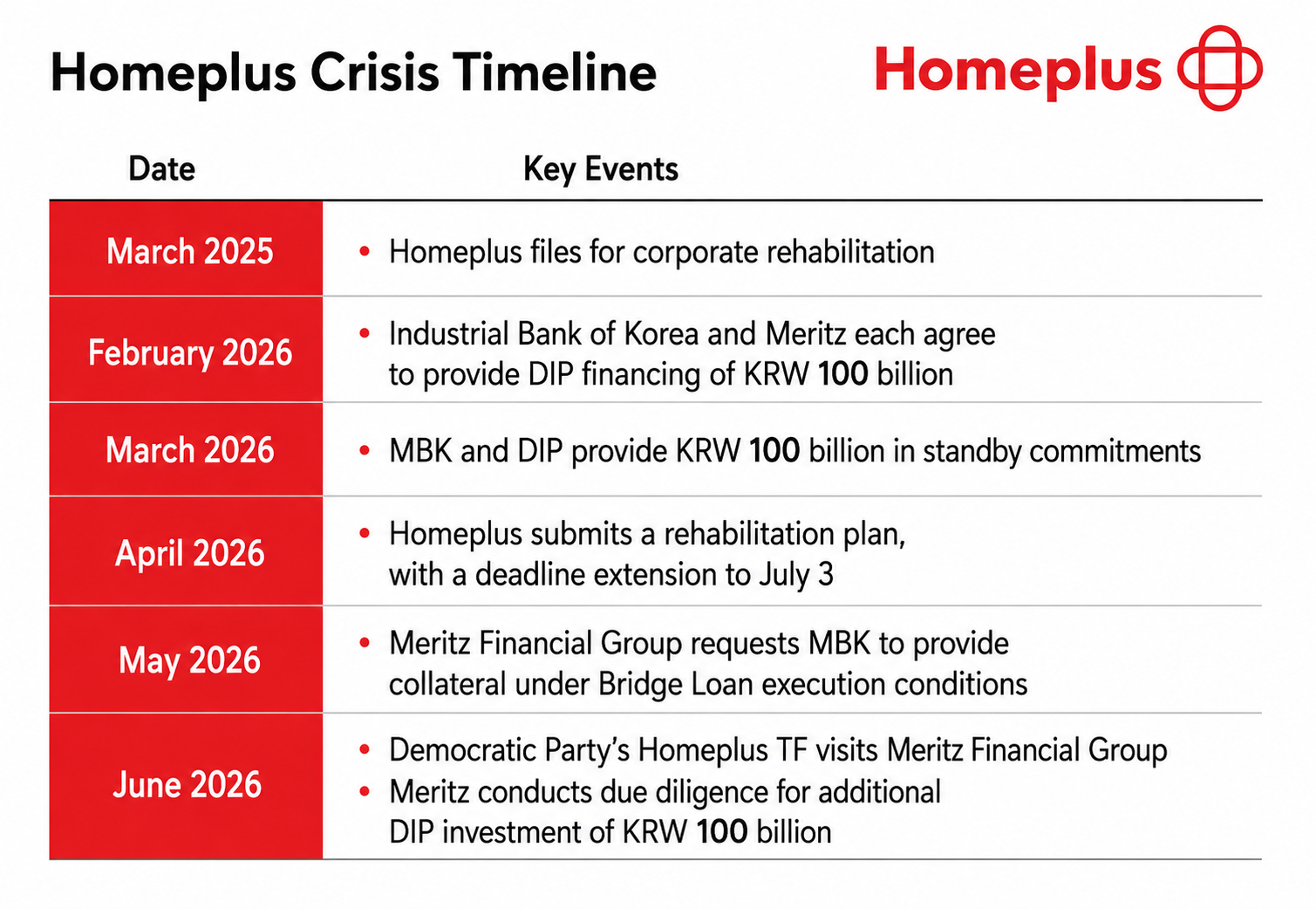

Since Homeplus entered court-led corporate rehabilitation in March 2025, the story has continued to evolve.

Most recently, public disagreements between Meritz Financial Group and MBK Partners

over who should bear the responsibility for the retailer's recovery have once again brought the case into the spotlight.

This is more than just the downfall of a major supermarket chain.

The Homeplus case brings together some of the most important concepts in corporate finance

—private equity, leveraged buyouts, corporate restructuring, and financial leverage.

Let's take a closer look at what happened and what investors can learn from it.

"The Decision Ultimately Depends on MBK Chairman Michael Kim"

Source: ESG Economy

Source: ESG Economy

On June 22, 2026, Meritz Financial Group announced

that it was willing to provide KRW 100 billion (approximately US$72 million)

in Debtor-in-Possession (DIP) financing to support Homeplus during its rehabilitation process.

Source: The Kyunghyang Shinmun (Korea)

However, the company stated that the financing would require guarantees

from MBK Partners and its chairman, Michael ByungJu Kim.

MBK Partners responded that it had already provided substantial financial support

and argued that the rehabilitation process is being managed under court supervision.

As both sides continue to exchange statements, one question remains:

How did Homeplus end up here?

Homeplus Was Acquired for KRW 7.2 Trillion

To answer that, we need to go back to 2015.

Source: Hans Economy

That year, Tesco decided to exit the Korean market and sold Homeplus to MBK Partners

for approximately KRW 7.2 trillion.

At the time, it was one of the largest M&A transactions in Korean history.

However, the business environment changed dramatically after the acquisition.

The rapid growth of e-commerce, combined with slowing demand

for traditional hypermarkets, placed increasing pressure on Homeplus.

On top of that, the acquisition itself had been financed with significant debt.

As financial burdens grew year after year, Homeplus eventually filed for court-led rehabilitation in March 2025.

To understand why, we first need to understand how private equity funds (PEFs) operate.

How Do Private Equity Funds Make Money?

Source: Naver News

A Private Equity Fund (PEF) invests in companies—often by acquiring controlling stakes—with the goal of increasing corporate value before eventually selling the business for a profit.

Simply put:

Buy a company. Improve it. Sell it at a higher valuation.

Two common strategies are frequently used.

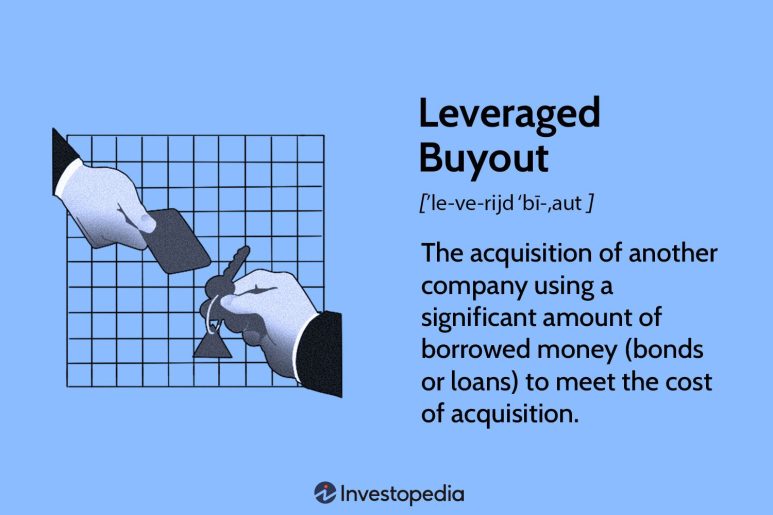

① Leveraged Buyout (LBO)

Source: Investopedia

A Leveraged Buyout (LBO) finances a large portion of an acquisition using borrowed money.

Rather than paying entirely with equity, investors rely heavily on loans.

The advantage is obvious:

- Less capital is required from investors.

- Larger acquisitions become possible.

The downside is equally significant.

The acquired company inherits substantial debt and interest expenses,

making future profitability much more important.

② Sale and Leaseback

Source: Access Working Capital

A Sale and Leaseback involves selling owned real estate while continuing to use it through lease agreements.

This provides immediate cash that can be used to repay debt or improve liquidity.

However, over time, rental expenses become recurring fixed costs.

Homeplus adopted this strategy by selling several store properties after the acquisition and using the proceeds primarily to reduce debt.

Why Did Homeplus Run Into Trouble?

Source: Financial News

The biggest challenge was that the market changed.

After 2020, e-commerce companies such as Coupang and Kurly grew rapidly,

fundamentally changing consumer shopping habits.

Traditional offline retail lost momentum.

Meanwhile, competitors such as E-Mart and Lotte Mart invested aggressively

in digital channels and store renovations.

Homeplus took a more conservative investment approach.

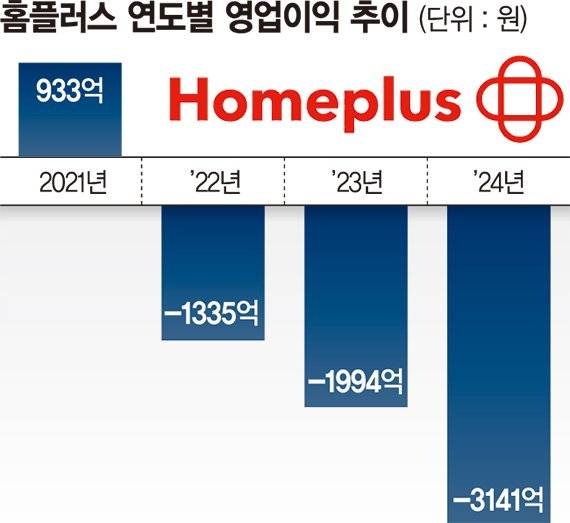

As a result, the company reported operating losses for three consecutive years (2022–2024)

while continuing to shoulder heavy debt obligations.

Ultimately, deteriorating fundamentals and financial leverage reinforced each other.

The Current Debate: Who Should Pay?

Now that rehabilitation is underway, the focus has shifted.

Rather than discussing operational recovery, the market is asking who should bear the financial burden.

The center of the debate is DIP financing.

DIP financing provides working capital to companies undergoing court-supervised

restructuring so they can continue operating.

Meritz Financial has expressed its willingness to provide funding but wants additional guarantees.

MBK maintains that it has already fulfilled its responsibilities.

Regardless of who is ultimately correct, the case highlights an important lesson:

The more stakeholders involved in a leveraged acquisition,

the more complicated accountability becomes during periods of financial distress.

Three Lessons for Investors

① Leverage Magnifies Both Returns and Risk

Debt can significantly improve investment returns when business conditions are favorable.

However, rising interest rates or weaker earnings can quickly turn leverage into a major liability.

The Homeplus case demonstrates how excessive debt can undermine long-term financial stability.

② Short-Term Cash Flow Is Not the Same as Long-Term Competitiveness

Businesses need continuous investment to remain competitive.

Investments in logistics, digital infrastructure, and store modernization may reduce short-term profits

but strengthen long-term growth.

Prioritizing only immediate financial performance can weaken future competitiveness.

③ Diversification Is Risk Management

The Homeplus rehabilitation affected not only shareholders but also suppliers, landlords, lenders,

and many other stakeholders.

It serves as another reminder that concentrating investments in a single company

or industry can expose investors to unexpected risks.

Learning Finance Doesn't Have to Be Difficult

News stories like Homeplus introduce unfamiliar concepts such as:

- LBO

- DIP Financing

- Sale & Leaseback

- Debt Ratios

Understanding how these concepts connect isn't always easy.

That's why many investors are turning to interactive learning formats such as quizzes.

In the Treasurer app, users can explore topics including market capitalization, PER, rebalancing, interest rates, and exchange rates through short, engaging financial quizzes.

In the Treasurer app, users can explore topics including market capitalization, PER, rebalancing, interest rates, and exchange rates through short, engaging financial quizzes.

Instead of memorizing financial terms, you can build practical investment knowledge one question at a time.

The Homeplus Story Isn't Over Yet

출처: Korea Zinc

The rehabilitation process is still ongoing, and the final outcome remains uncertain.

Regardless of how it ends, the Homeplus case will likely remain one of Korea's most important examples of

how private equity, leveraged buyouts, corporate restructuring, and financial leverage interact in practice.

Economic news is more than headlines—it offers valuable insights into investing, corporate finance, and risk management.

We'll continue breaking down major financial stories into practical lessons for investors.

🌐 Related Articles